Understanding The Differences Between GAAP And Statutory Accounting

In the world of accounting, understanding the various frameworks that guide financial reporting is essential for businesses and stakeholders alike. One of the most significant distinctions lies between Generally Accepted Accounting Principles (GAAP) and statutory accounting. Each of these frameworks serves unique purposes and caters to different audiences, making their understanding vital for accurate financial representation. As organizations navigate the complexities of financial reporting, they must choose the appropriate accounting framework that aligns with their objectives and compliance obligations. This choice not only impacts how financial information is presented but also how it is interpreted by investors, regulators, and other stakeholders.

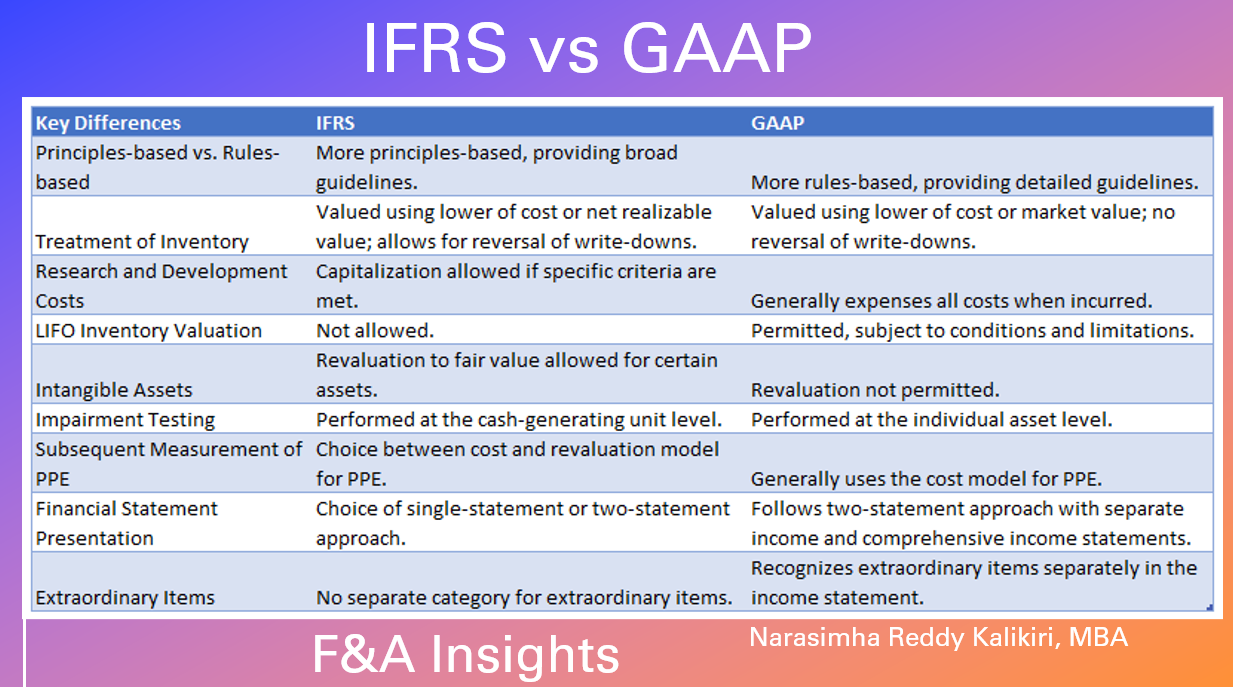

The decision between GAAP vs statutory accounting often leads to confusion, especially for those new to the field. GAAP is a set of rules and standards established by professional accounting bodies, primarily in the United States, aimed at ensuring consistency and transparency in financial reporting. On the other hand, statutory accounting refers to the legal requirements specific to a jurisdiction, often tailored for regulatory bodies and aimed at safeguarding public interest. Understanding the nuances of both frameworks can empower organizations to make informed decisions about their financial reporting practices.

As we delve deeper into GAAP vs statutory accounting, we will explore their definitions, key differences, and implications for businesses. By the end of this article, readers will have a comprehensive understanding of both accounting frameworks, allowing them to navigate the financial reporting landscape with confidence and clarity.

Read also:Bellossom The Vibrant Evolution Of Natures Charm

What is GAAP?

Generally Accepted Accounting Principles (GAAP) is a collection of commonly-followed accounting rules and standards for financial reporting. These principles are formulated by the Financial Accounting Standards Board (FASB) in the United States and are designed to ensure consistency, reliability, and transparency in financial statements. GAAP encompasses a wide range of concepts, including revenue recognition, balance sheet classification, and the matching principle. By adhering to GAAP, businesses can provide stakeholders with a clear and accurate picture of their financial performance and position.

What is Statutory Accounting?

Statutory accounting refers to a set of accounting practices that are mandated by law or regulation within a particular jurisdiction. This framework is often utilized by entities that are subject to regulatory oversight, such as insurance companies and banks. Statutory accounting focuses on the solvency and financial stability of an organization, ensuring that it meets the necessary legal requirements. Unlike GAAP, which aims to present a true and fair view of financial performance, statutory accounting is primarily concerned with compliance and protecting the interests of policyholders and creditors.

How Do GAAP and Statutory Accounting Differ?

The differences between GAAP and statutory accounting are significant, and understanding these distinctions can help organizations choose the right framework for their needs. Here are some key differences:

- Purpose: GAAP focuses on providing a true representation of an entity's financial performance, while statutory accounting emphasizes compliance with legal regulations.

- Flexibility: GAAP offers more flexibility in accounting methods, allowing companies to choose the approach that best suits their operations. Statutory accounting, however, is often rigid and prescriptive.

- Reporting Frequency: GAAP typically requires quarterly and annual financial statements, whereas statutory accounting may have different reporting requirements based on regulatory needs.

- Audience: GAAP is primarily aimed at investors, analysts, and other stakeholders, while statutory accounting caters to regulators, policymakers, and creditors.

Why is GAAP Important for Businesses?

GAAP plays a crucial role in the business environment, providing numerous benefits to companies that adhere to its principles. Some of the key reasons why GAAP is important include:

- Enhances Credibility: By following GAAP, businesses can enhance their credibility and trustworthiness among investors and clients.

- Facilitates Comparability: GAAP ensures that financial statements are prepared consistently, making it easier for stakeholders to compare the financial performance of different entities.

- Reduces Misinterpretation: A standardized accounting framework minimizes the risk of misinterpretation of financial data, leading to better decision-making.

- Attracts Investment: Companies that adhere to GAAP are often more attractive to investors, as they provide a clearer picture of financial health.

What Are the Limitations of GAAP?

While GAAP offers numerous advantages, it is not without its limitations. Some challenges associated with GAAP include:

- Complexity: GAAP can be complex and difficult to navigate, particularly for smaller businesses without dedicated accounting resources.

- Potential for Manipulation: Although GAAP aims for transparency, there is still room for manipulation, as companies may exploit loopholes to present a more favorable financial position.

- Costly Compliance: Adhering to GAAP can be expensive, especially for smaller businesses that may struggle to meet the compliance requirements.

Why is Statutory Accounting Necessary?

Statutory accounting serves a vital purpose in ensuring the financial stability and compliance of regulated entities. Here are some reasons why statutory accounting is necessary:

Read also:Dallas House Of Blues A Unique Live Music Experience

- Protects Stakeholders: Statutory accounting practices are designed to protect policyholders and creditors by ensuring that companies maintain sufficient reserves and solvency.

- Ensures Regulatory Compliance: By adhering to statutory accounting requirements, businesses can avoid legal penalties and maintain their operating licenses.

- Enhances Financial Stability: Statutory accounting promotes financial stability by ensuring that companies meet their obligations and maintain adequate financial reserves.

What Are the Challenges of Statutory Accounting?

Despite its importance, statutory accounting also presents several challenges, including:

- Rigidity: The prescriptive nature of statutory accounting can be restrictive, making it difficult for companies to adapt their financial reporting to changing business environments.

- Limited Flexibility: Unlike GAAP, statutory accounting offers limited flexibility in accounting methods, which may not accurately reflect a company's financial position.

- Complex Regulations: Navigating the complex regulations and requirements of statutory accounting can be challenging, particularly for entities operating in multiple jurisdictions.

GAAP vs Statutory: Which Should You Choose?

The choice between GAAP and statutory accounting ultimately depends on the nature of the business and its regulatory obligations. Companies that are publicly traded or seeking investment may find GAAP to be the more suitable framework, as it enhances credibility and provides a clearer picture of financial performance. On the other hand, regulated entities such as insurance companies or banks must adhere to statutory accounting to meet legal requirements and protect stakeholders.

In conclusion, understanding the differences between GAAP vs statutory accounting is essential for businesses navigating the complexities of financial reporting. By choosing the appropriate framework, organizations can ensure compliance, enhance transparency, and ultimately foster trust among their stakeholders.

Article Recommendations